You have NSOs to exercise, or shares from a past NSO exercise to sell. Six expensive mistakes wait between grant and sale: five at exercise, one at sale. Two stand out by dollar impact: the cost-basis adjustment when selling the shares, and the calendar-year timing of the exercise itself. Each can save four to six figures on a typical grant.

On a typical NSO grant, four to six figures depends on two decisions easy to miss without a checklist.

The six most expensive NSO mistakes

If you read nothing else, read this. These are the traps that cost real money, ordered by how often they're missed.

- Double-paying tax on the same gain when you sell the shares. When you sell shares from a past NSO exercise, your broker's 1099-B reports your cost basis as just the strike price (per IRS Form 1099-B Instructions), leaving out the bargain element you already paid ordinary tax on at exercise. Without a one-line adjustment on Form 8949 (column g, code B), you'll pay capital-gains tax on it a second time. On a $300K bargain, that's $45K-$75K of overpayment. Full mechanics below.

- Exercising in the wrong calendar year. If you're about to retire, take a sabbatical, switch to a lower-paying role, or take a career break, exercising in the high-income year instead of the low-income year leaves tens of thousands of dollars on the table. The bargain element stacks on your other income; exercising on $50K of retirement income vs $400K of salary can be the difference between the 22% bracket and the 35% bracket on most of the gain.

- Treating your employer's withholding as your final tax. The IRS flat supplemental rate (currently 22% per IRS Pub 15) is well below most tech employees' marginal bracket. On a $300K bargain element, the gap you owe at filing easily runs $30-50K. Plan estimated payments or sell extra shares immediately. The catch if you don't: the IRS charges underpayment interest (currently around 8% annualized) on the shortfall, accruing from the relevant quarterly due date until you pay.

- Cash-funding the exercise without the cash. Strike plus tax on a typical grant easily clears six figures. If the stock drops afterward, you're stuck with tax owed in cash on shares worth less. Sell-to-cover is the safer default unless you have both the cash and high conviction.

- Triggering FICA when you don't have to. Exercising NSOs as a W-2 employee triggers Medicare (1.45%, plus 0.9% above the additional-Medicare threshold) on the bargain element. Exercising after departure (within the post-departure exercise window your grant allows, typically 90 days but sometimes longer) skips it. On a $1M-plus bargain element that runs $14K-$25K in savings, scaling linearly with grant size. Covered in the "FICA savings on the way out" section below.

- Holding for LTCG with already-heavy concentration. The long-term rate discount is real, but so is the single-stock risk you're adding. If your existing position in the company is already large, the marginal gain from the LTCG discount may be smaller than the marginal cost of the added exposure. See it in dollars below.

For a deeper walk-through of how to think about concentration risk, see the single-stock concentration risk article.

What exercising actually triggers

On the day you exercise, the gain (current share price minus your strike, times shares) gets treated as ordinary income. Not capital gains. Not AMT. Not NIIT. Plain wages. It shows up on your W-2 just like a bonus would, and it's hit by federal income tax at your marginal rate, state income tax, and FICA. In a high-tax state like California, up to about 53% of the gain can go to tax (37% federal + 13.3% state + 2.35% Medicare at top brackets).

Two things to know about the withholding side. Your employer will under-withhold at the flat supplemental rate (currently 22%), not at your actual marginal bracket. The gap becomes federal tax owed at filing time. (Same dynamic on RSU vests; the RSU withholding gap article covers four ways to close it.) High-tax states compound the bill: CA, NY, NJ, and OR all stack 10%+ state income tax on top.

Decision one: cash-fund or sell-to-cover

Exercising costs cash for two things: the strike price, and the tax bill. You can pay both from your own savings (cash-fund), or have the broker sell some of the freshly-exercised shares to cover them (sell-to-cover). The tax bill is the same either way. The only thing that changes is how many shares you walk away with.

| Cash-fund | Sell-to-cover | |

|---|---|---|

| Cash out of pocket | Strike + tax bill (often six figures) | $0 |

| Shares you keep | All of them | Fewer (broker sells enough to fund the cash) |

| Best when | You have the cash AND high conviction | You don't have the cash, or conviction is soft |

The trap with cash-fund: if the stock drops after you exercise, you're holding shares worth less than the cash you just put up. Sell-to-cover is the safer default for most situations.

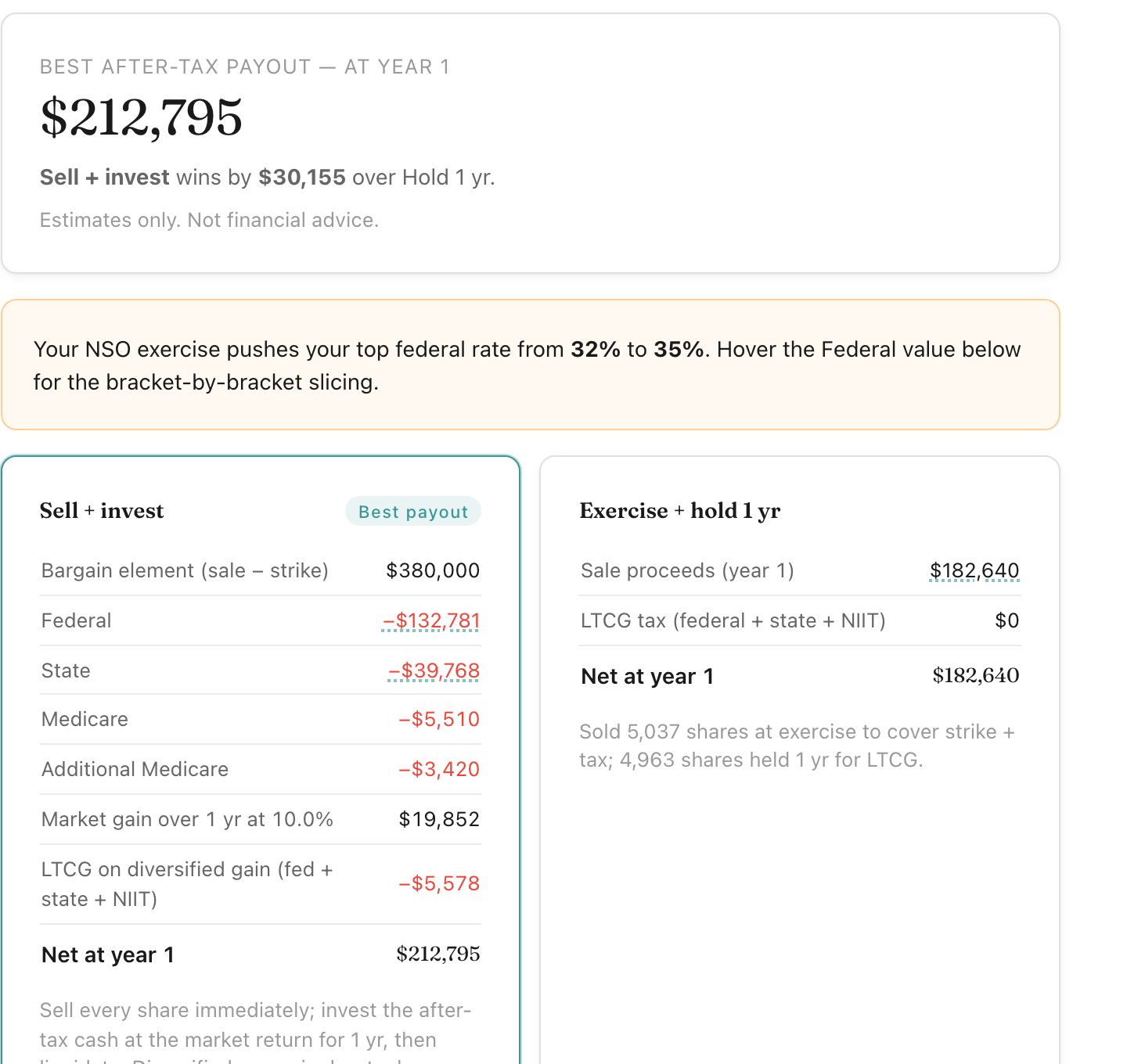

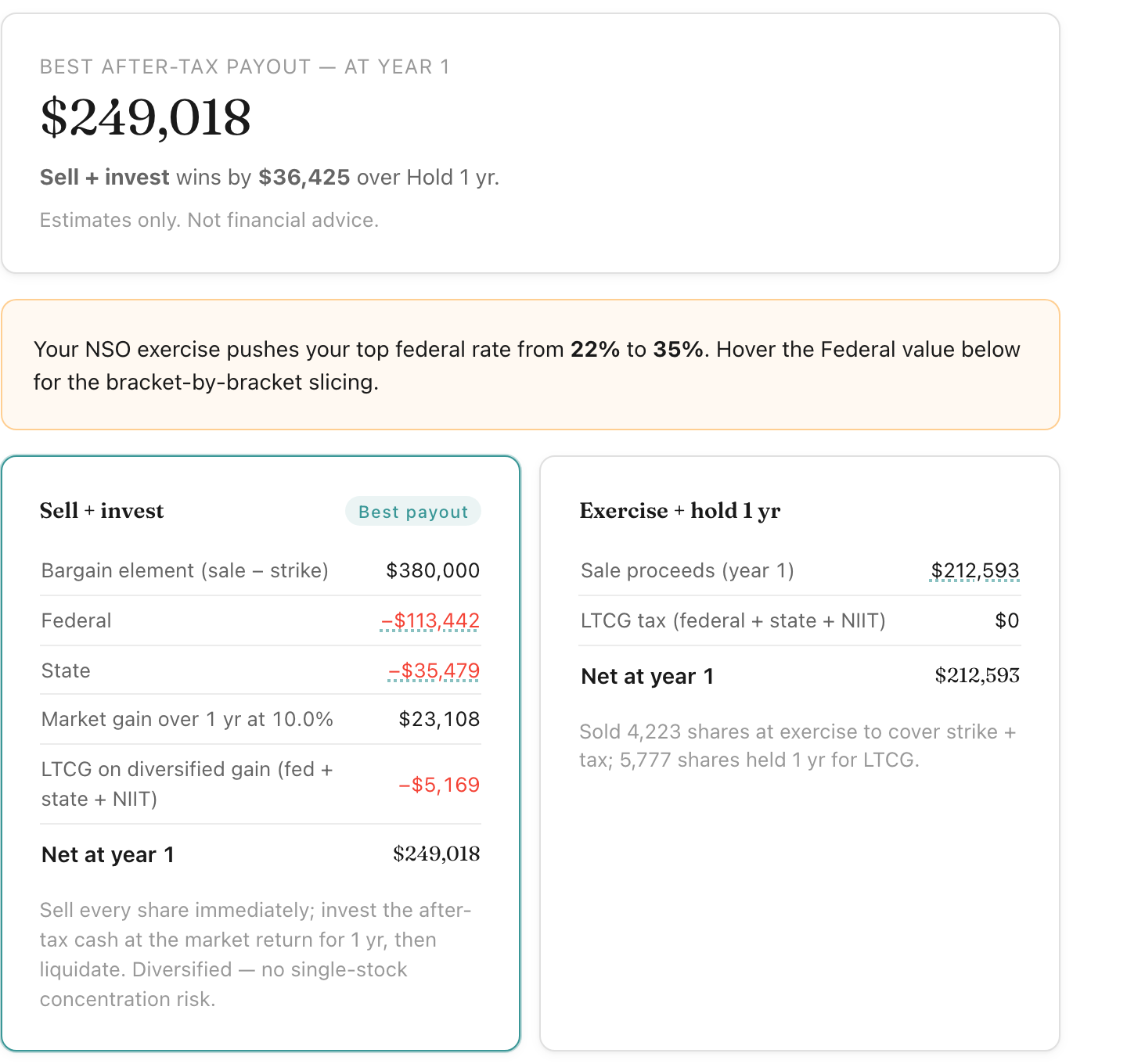

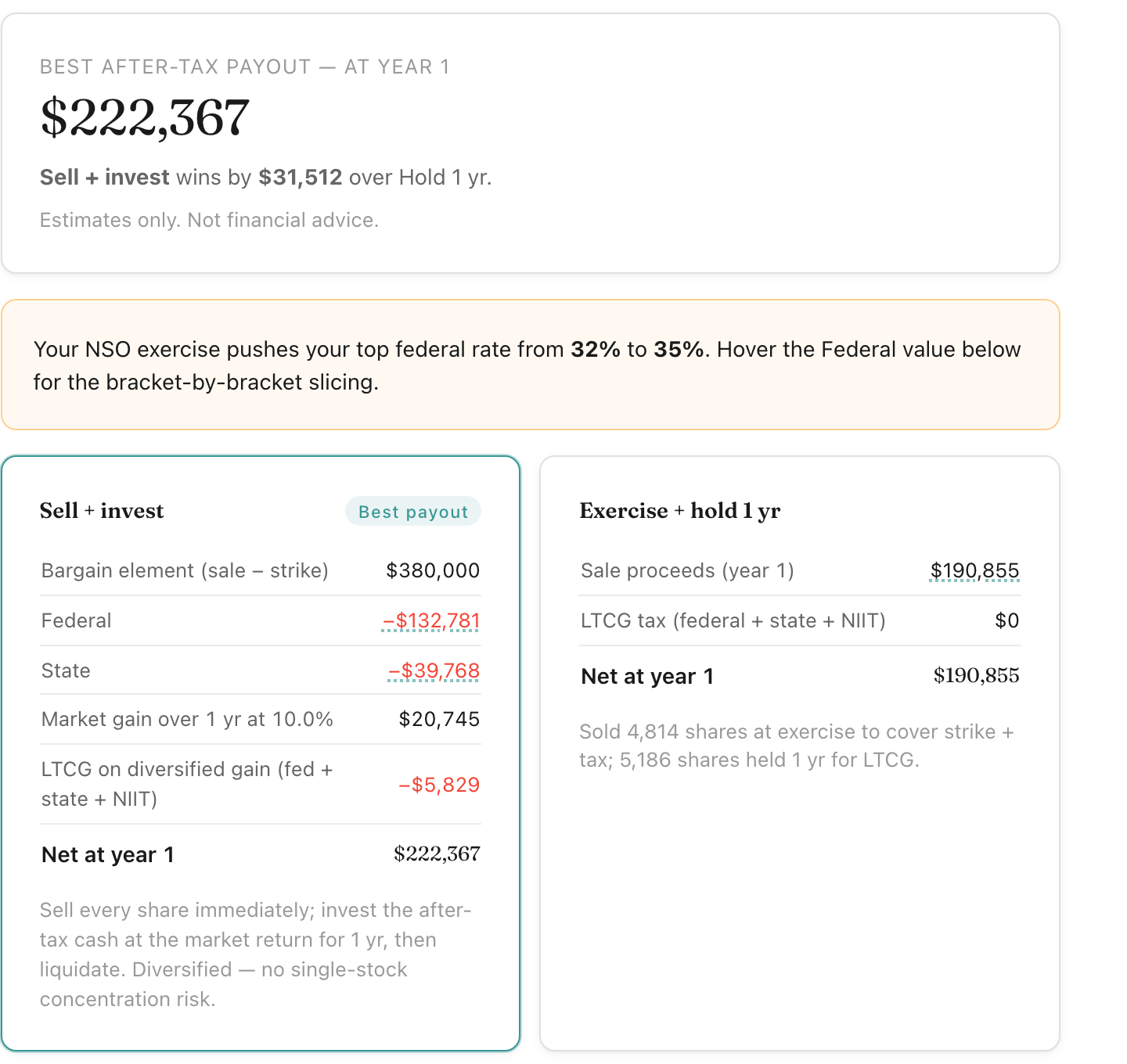

Decision two: sell at exercise, or hold for the long-term rate

After exercise, your cost basis is the current price. Selling immediately captures the gain at ordinary rates and closes the position. Holding lets you reach the long-term capital-gains rate on any appreciation above that basis, after a 12-month holding period.

The LTCG-rate discount is real (top federal ordinary is currently 37%, top LTCG is 20%, with 3.8% NIIT layered on top of capital gains either way). But the discount only kicks in on appreciation above your basis. If the stock stays flat or drops, holding gives nothing back and locks in concentration risk you don't need.

Sell at exercise is the right call when:

- You already hold meaningful single-stock exposure in the same company (typical for tech employees with RSUs and ISOs from the same employer)

- Your conviction in continued upside is soft

- You need the cash for the tax bill, a near-term purchase, or simple diversification

- The stock's expected return doesn't clearly beat the broad market on a risk-adjusted basis

Hold for 12 months is the right call when:

- You have genuine conviction the stock will outperform the broad market over the next 1-3 years

- Position size is small enough that the added concentration risk is acceptable

- You can fund the exercise from cash (otherwise you've already given back half the upside through sell-to-cover)

If you hold, you can also hedge. A protective put (or a zero-cost collar that funds the put by selling a call above the current price) locks in your downside through the 12-month LTCG window without forcing you to sell. Worth pricing if your conviction is high but you can't stomach a 30-50% drawdown on the position while you wait for long-term treatment.

The five-figure basis adjustment most filers miss

This is the most expensive trap and the easiest to fix. It only applies if your exercise had a bargain element (current share price was above your strike). If you early-exercised at strike = current price with a §83(b) election, or otherwise exercised with no bargain element, your broker's basis is already correct and the rest of this section doesn't apply to you.

For NSO shares acquired through an exercise that had a bargain element, your true cost basis is the strike you paid plus the bargain element you were taxed on as ordinary income the year you exercised. The bargain element already showed up on your W-2 (box 1) and you paid federal + state + FICA on it at that time. So when you sell the shares later, you should only owe capital-gains tax on appreciation above the share price at exercise. Not on the full distance from the strike.

The problem: IRS basis-reporting rules (effective for shares acquired on or after January 1, 2014) direct brokers to report your cost basis on Form 1099-B as only the strike price. Not strike plus bargain element. The underlying authority is Treasury Regulation §1.6045-1(d)(6)(ii)(B), and the IRS Form 1099-B Instructions make it explicit: "You cannot increase initial basis for income recognized upon the exercise of a compensatory option or the vesting or exercise of other equity-based compensation arrangements granted or acquired after 2013."

The fix is on your side, and the IRS spells it out in the Form 8949 Instructions: "For compensatory options granted after 2013, the basis information reported to you on Form 1099-B... won't reflect any amount you included in income upon grant or exercise of the option. Increase your basis by any amount you included in income upon grant or exercise of the option." The mechanic is a one-line adjustment in column (g) with code B. Many tax software products and tax advisors don't flag this automatically; the safest path is to look at the supplemental statement from your exercising broker (it shows the adjusted basis or the ordinary income recognized at exercise) and make sure that number is used as your basis on Form 8949, not the Form 1099-B basis.

The fix: when you sell shares from an NSO exercise, locate the supplemental statement from the exercising broker (Schwab Stock Plan Services, E*TRADE Equity Edge, Morgan Stanley Shareworks, etc.). It will show the "adjusted basis" or "ordinary income recognized" alongside the 1099-B basis. That's the number you add to your cost basis on Form 8949. The IRS gets a copy of your W-2 with the bargain element already in it; their systems match the adjustment you make. You're not getting away with anything; you're just claiming the basis you already paid for.

Time the exercise to the right calendar year

Calendar timing is the planning lever with the biggest dollar swing, and it only shows up if you treat exercise as a multi-year question instead of a calendar-year reaction. The next two sections walk through how.

Wait until next year if a low-income year is coming

Your NSO bargain element stacks on top of whatever other ordinary income you have that year. If you're about to retire, take a sabbatical, switch to a lower-paying role, or take a career break, exercising in the high-income year (this year) instead of the low-income year (next year) can leave four to six figures on the table.

Why it works: ordinary-income tax is bracketed. In the high-income year, your $380K bargain element stacks on top of $250K of salary and lands almost entirely in the 35-37% bracket. In the low-income year, the same bargain element starts lower in the ladder and a large share of it is taxed at 22-24% instead. Same gain, different bracket structure, materially different outcome.

The trade-off:

- You have to actually wait. If the stock moves significantly before then, the timing savings can be wiped out by a price move.

- The grant has to still be exercisable then. If you're planning around departure, your post-departure exercise window is the binding constraint. Check yours before deferring.

Exercise after departure to skip FICA

Here's a planning detail almost no one mentions: FICA only applies to NSO exercises while you're still a W-2 employee of the issuing company. Exercise after departure, but within the post-departure exercise window your grant allows (typically 90 days; sometimes longer), and you owe federal income tax and state income tax on the bargain element, but not FICA.

Social Security stops at the annual wage base (around $176K for 2025), which most equity holders blow past on regular salary alone, so the Social-Security side is usually maxed out either way. The savings is the Medicare component (currently 1.45% on everything, plus 0.9% above the additional-Medicare threshold), which scales linearly with the bargain element.

Two moves combined

For someone retiring at year-end with a typical NSO grant, both moves compound: exercise after your last day on the W-2 (skip FICA) AND in the following calendar year (drop into a lower bracket). In the scenario above, the combined savings runs $35K-$45K on a $380K bargain, with no change in the underlying decision to exercise.

Where to go from here

For your specific grant, the NSO Exercise Calculator runs the tax math on your inputs and compares cash-fund vs. sell-to-cover and sell-at-exercise vs. hold (up to 10 years) side by side.

If you also have ISOs at the same company, the AMT crossover on those is usually the bigger lever. If exercising leaves you with more single-stock exposure than you can comfortably hold, the concentration risk article walks through the de-concentration playbook.

The calculators here handle one decision in isolation. OptionsAhoy plans the full picture jointly: every ISO, NSO, RSU vest, concentrated position, and hedge, across bullish, neutral, and bearish scenarios. The output is a year-by-year Plan optimized for total after-tax wealth. Free during beta.

Common questions

What is the total tax I pay on a non-qualified stock option exercise: federal, state, FICA, and Additional Medicare?

At exercise the bargain element (shares times the difference between fair market value and strike) is taxed as ordinary compensation: federal income tax, state income tax, Medicare, the 0.9% Additional Medicare surtax, and Social Security if you are below the annual wage base. For 5,000 options with a $40 bargain element ($200,000 total) on $200,000 of salary in California, that is roughly $68,200 federal, $18,900 California, $2,900 Medicare, and $1,800 Additional Medicare, about $91,800 or 46% of the bargain element (Social Security was zero here because the salary already exceeded the wage base). The NSO calculator returns the line-by-line stack for your inputs.

Educational content for general information, not personalized tax, legal, or financial advice. Consult a qualified professional for your specific situation. See Terms.